Scalability

Mass customer acquisition, retention and profit

scale with one thing:

how many business operations you control.

AI is built on top of this layer.

Horizontal scalability: ~33M (EU) → ~400M globally addressable micro clients

Vertical scalability: 12 revenue-generating points per micro-client

Your goal:

- mass client acquisition and preventing churn

- profit maximization

Ordware UBOS provides a solution for this.

Strategy:

Buy the Ordware system source code > adapt it to your own branding > give it free to the bank’s clients > harvest the benefits.

What scalability really means

Scalability is not only about how many clients you reach, but how deeply you are embedded in their operation.

Horizontal scalability

It answers the question of how many clients can be acquired with Ordware.

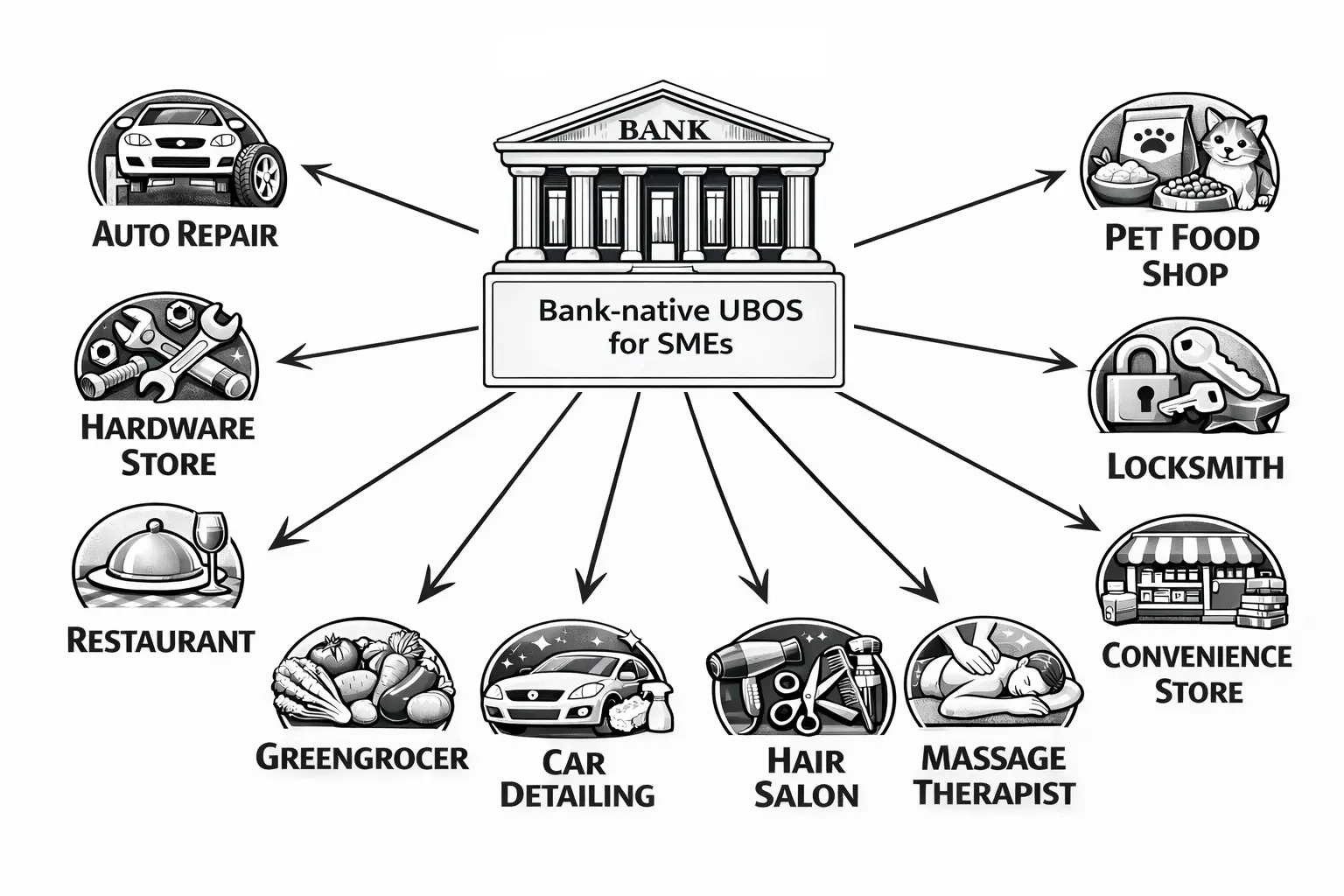

The system is universal. It satisfies the digitalization needs of micro-businesses, therefore the size of the target group is enormous.

Examples from the target group:

Greengrocer, hospitality business, screw shop, auto repair workshop, pet food retailer, car detailing business, hairdresser, massage therapist, small grocery store, locksmith workshop, etc.

This is the foundation of vertical scalability.

Scalability

After a single registration, the client receives all of the listed functions, but only uses what they need.

Horizontal target group and size:

- target group: micro businesses in the European Union

- size: as a rule of thumb, there are roughly 9 micro businesses per 100 inhabitants

- this is broadly true across Europe

- there are approximately 33 million businesses in the European Union

In terms of horizontal scalability, both EU and non-EU markets can be reached with Ordware, but in assessing the average annual turnover of the targetable micro-businesses, it is worth taking into account both the activity of the target group and the level of development of the market.

It is worth treating Hungary as 1 unit and multiplying upward by development level.

In Hungary there are approximately 900,000 micro businesses.

Together, they generate approximately USD 62+ billion in revenue.

This is the gross economic space, layer, and field over which the bank can exercise control with Ordware in Hungary.

By development level:

Tier1, Tier2, Tier3

By activity:

Massage therapist, retail unit, hospitality business, etc.

The multiplication of these gives the gross horizontal scalability in a given market.

Vertical scalability

For a given client and business activity, in how many places can fees and commissions be collected, and at what scale?

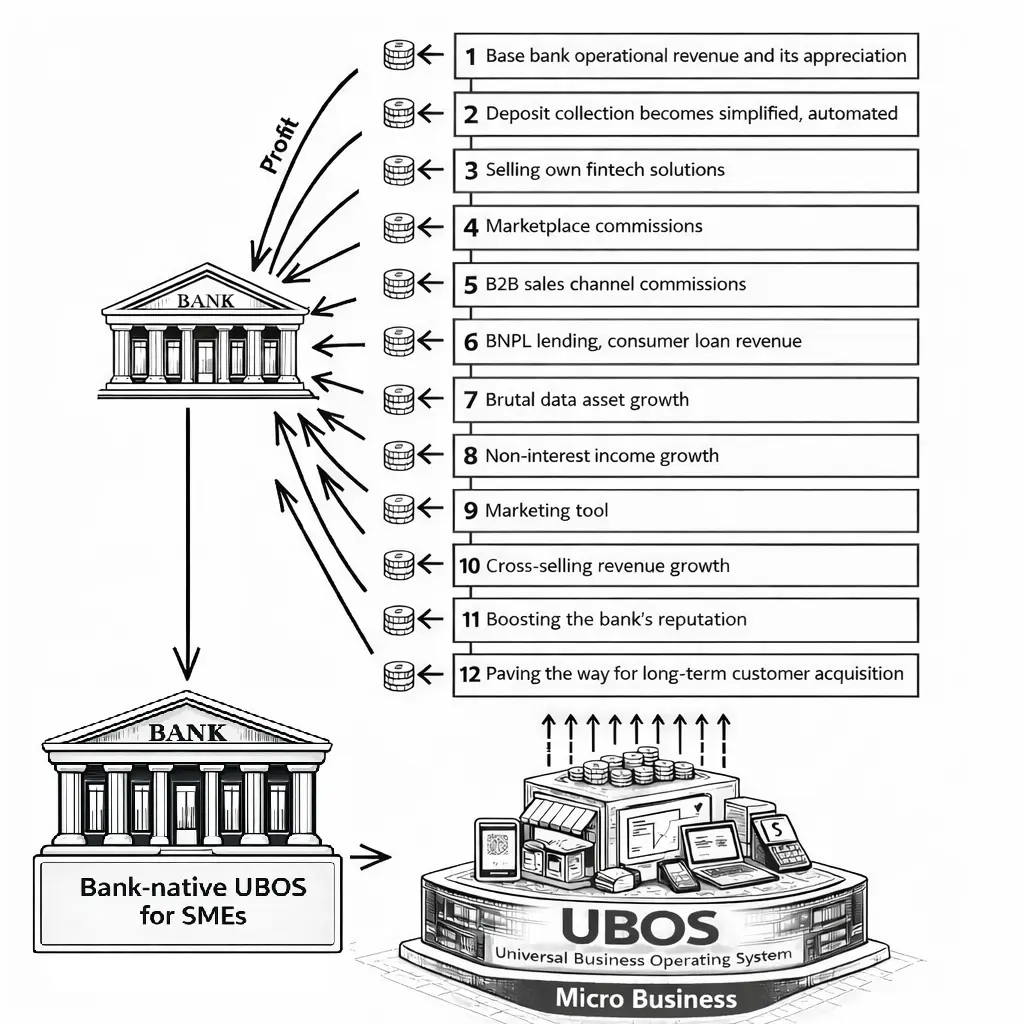

Revenue-generation points in the Ordware profit engine:

- Core banking revenue and the revaluation of those revenues

- Deposit collection becomes simpler and automatic

- Sale of own Qvik, online, and other payment and fintech solutions

- Marketplace commissions

- B2B sales channel commissions

- BNPL lending and consumer loan revenues

- Brutal growth in data assets – lending and risk assessment improve

AI foundation → see Control & Intelligence - Growth in non-interest income

- Expansion of the bank’s marketing and communication surface with society

- Growth in cross-selling revenue

- Increases the bank’s reputation

- Lays the foundation for long-term client acquisition

Profitengine

Scalability defines how big the opportunity is.

The Profit Engine defines how it is monetized.

1. Core banking revenue

Monthly account maintenance fees, accounting fees, transfer commissions, cash handling commissions, payment commissions, etc.

If the client base grows through Ordware, these core fees are generated.

The basis of their revaluation is that if the client receives the system free from the bank, then the bank applying higher pricing becomes fundamentally acceptable from the client’s point of view, and price competition disappears.

For example:- higher account maintenance fee: monthly USD 31.25 instead of USD 15.625

- higher transfer commission: for example 0.13% instead of 0.1%

- higher payment commission: not IC++ 0.8–1%, but 1.2–1.4%, etc.

2. Deposit collection becomes simpler and automatic

This is fundamentally banking revenue, but it is worth handling separately, because a deposit is not a fee, but “raw material,” funding, for the bank.

As a rule of thumb, every business keeps approximately 10% of its annual turnover in its current account as liquidity.

By giving the system free to its clients, the bank automatically solves part of its deposit collection task.

Part of this funding base becomes the basis for bank lending. Its yield is therefore the BUBOR.

3. Sale of own Qvik, online, and other payment and fintech solutions

Because the bank gives its own operating system to the micro-business, it can provide its own payment solutions within it.

There is no profit-sharing.

All revenue belongs to the bank.

4. Marketplace commissions

This is a type of revenue to which the bank previously had no access. The micro-business receives its ordering interfaces from the bank: webshop, ordering applications, etc.

At the end of the purchase flows, the payment solution will be the bank’s solution, but since the ordering interfaces are also provided free by the bank, the bank does not need to maintain or operate them for direct commercial gain in the traditional sense, only collect the benefits, therefore the bank can rightfully charge a commission to the micro-business.

As a comparison:Fizz.hu, eMag, Amazon, eBay, etc. also charge commissions to those who sell through their systems. Ordware offers a better solution than these, because with Ordware the bank can collect commissions not only on products sold electronically in a “classic” marketplace sense, but even on a single fried dough item, or a beer ordered to a table.

5. B2B sales channel commissions

This is what turns the bank into a market organizer and sector-governing actor.

Illustrated with an example:

If the bank has given the system free to 1,000 hospitality businesses, then it can speak to 1,000 hospitality businesses at once.

The hospitality business not only sells, but also buys. It buys raw materials. It buys these from suppliers of hospitality products (HORECA suppliers).

For a fee or commission, the bank allows the HORECA supplier to reach its client through a procurement function. This is a sales channel for the HORECA supplier, so they are happy to pay in order to be included.

This is not about the bank starting to sell chicken meat. It is about the fact that if the bank owns the value chain, then if business is concluded through it, it is justified in asking for money for it.

The scale of this is explained in the Profit Engine section.

6. BNPL lending and consumer loan revenues

The basis for this is that the bank provides not only the banking relationship but also the electronic and ordering interfaces of its Ordware-using client.

Therefore, purchases made through those interfaces are directed by the bank.

As a result, the bank can sell BNPL or other consumer credit products at the moment of purchase.

7. Brutal growth in data assets – lending and risk assessment can improve and accelerate

The bank’s dream.

The bank sees every economic event.

It sees what the client sold, at what hour and minute. It sees the size of its inventory, the stock levels it operates with. It sees which payment instrument was used. It sees what was consumed at which table, what was delivered where, and who the customer was.

Thus, at every moment, it sees the operation of its client with perfect precision.

It sees the client’s entire operation minute by minute, as well as the historical data.

This supports immediate risk assessment and loan underwriting.

AI foundation → see Control & Intelligence

8. Growth in non-interest income

The system is universal in terms of micro-business needs, but this does not mean that every client must be offered the same functions.

The system is highly configurable and, in terms of function depth and solutions, can be customized and parameterized for a given business or business type.

- • There is ample room to decide which functions are given free and which are charged separately.

- • The client-retention goal is already achieved if the bank gives Ordware, or part of it, for free, but< dependency and attractiveness can be increased further if the bank also provides the related tools either free or for a fee./li>

9. Expansion of the bank’s marketing and communication surface with society

A banking marketing dream.

Sales messages become simplified. Easy, simple, clear messages.

“Come to us and you will receive salvation.”

Client acquisition and retention become simpler.

Communication with society becomes simpler.

Noise independence and media independence can be achieved through this, because the bank also provides the sales interfaces of the micro-business, so the customers of the micro-business see a surface that contains the bank’s unique design elements and name, therefore this becomes a free, proprietary communication surface.

10. Growth in cross-selling revenue

On this free communication surface, the bank can also promote and sell its other products.

11. Increases the bank’s reputation

The bank as savior.

Because the system in itself solves the digitalization problem of micro-businesses, the bank can reposition itself through it.

It is not only “taking the micro-business’s money,” but creating value, helping, and supporting.

12. Lays the foundation for long-term client acquisition

Because this system is cloud-based and tied only to a registration, the cost of serving each new user is almost zero.

The bank can provide the most modern system in existence to public education and vocational training as support.

This can further increase its reputation, but more importantly, students graduating from commerce and hospitality training, secondary schools, and vocational schools will leave these institutions having been socialized on the bank’s system, having come to know it, and having learned it.

Thus the new workforce entering the market:

- can influence their employer at the workplace to switch to the bank’s system

- and the next entrepreneurial generation will build on the bank’s system